✒️#15 - Uno Reverso!

✒️#15 - Uno Reverso!

Reverse brainwashing, reverse fund-of-funds

Good morning!☀

Here's your weekly roundup of the most interesting things I've read, learned, or listened to. I write about the people and funds that can create a better world for us.

Enjoying the newsletter? Share it with somebody you like. No supply chain issues here.

🔮How do you un-brainwash somebody?

In 2020, Melissa Rein Lively went viral for filming herself going berserk - destroying mask displays in a Target. Not as feverishly reported is that, a few months before the freakout, she published an article calling on the Scottsdale mayor to put more stringent COVID protection policies in place.

From QAnon to cult activities to Nazism, people have done or said things they later realized didn’t embody their actual beliefs. How do they come to so deeply embody a radical ideology? Gentle nudges that reinforce a particular viewpoint and incrementally narrows mindsets. People don’t become polarized quickly, they become polarized slowly.

Reasoning will never make a Man correct an ill Opinion, which by Reasoning he never acquired - Jonathan Swift

Put another way: you can’t reason somebody out of something they didn’t reason themselves into. People who so deeply believe something will generally not be swayed by logic. That’s science my friends, not me. We’ve all been victim to this on both sides. Kicking a dead horse as we hurl logic at a distant relative who just refuses to acknowledge fact. Or being presented with logic and fact by our spouse and just thinking “nah.”

How does this relate to our everyday lives? We interact with nudges everyday. Every platform through which we view content uses algorithms designed to help us find more things that we enjoy faster. Netflix, Prime, Twitter, Facebook, Google, YouTube. Even Instacart and Uber Eats. It’s convenience. Hooray!

But when it comes to information we consume, we end up only reading, listening to, or watching things related to content we’ve already read, listened to, or watched. In essence, content that we like. Things we want to hear. Uh oh. There’s that gentle nudging. And when everybody becomes more polarized, individuals feel more isolated from one another, leaving them even more vulnerable to further nudges.

Uber Eats isn’t trying to brainwash you into ordering from that one Italian restaurant (I think). But this type of behavior is very clearly an unintended consequence of convenience algorithms. So if we are all slowly believing a narrower set of beliefs more fervently than ever before, how do we pull out of this tailspin? How do we reverse-brainwash ourselves?

There are two scientifically effective ways to release the vice jaws of polarization. One way is very simply engaging with others. Showing compassion to people we disagree with. Conversing and, sure, debating. But debating the ideas, not the people. The second way is showing people their peers who have alternative points of view. If I see somebody who shares my core values is more open to alternative perspectives on a given topic, I too will be more open to alternative perspectives.

This is actually what Parler was built to do. If you listen to the founders John Matze and Jared Thomson describe their vision, they point to the namesake - parler is French for to converse. Their dream was an app that encouraged debate. Somebody would post something, much like on Twitter, and then people on both sides of the conversation would engage. That’s of course not how Parler is known. It’s known as a catchment area for one particular extreme. For that, it was, for a time, erased from the internet by Amazon and Apple.

So what role do preference algorithms play in our societal behavior? An absolute and inseverable role. Do platforms creating these algorithms have a responsibility to mix things up so as to not nudge us to polarization? Morally, probably. Should we force them to? No. Are we all lost? Also no.

Everybody is vulnerable to sitting passively as content is chosen for us. However, everybody also has the capability to actively choose what you watch, listen, and read. To actively seek out alternative points of view. It takes more effort, sure. But it’s better than a dumpster fire of a society.

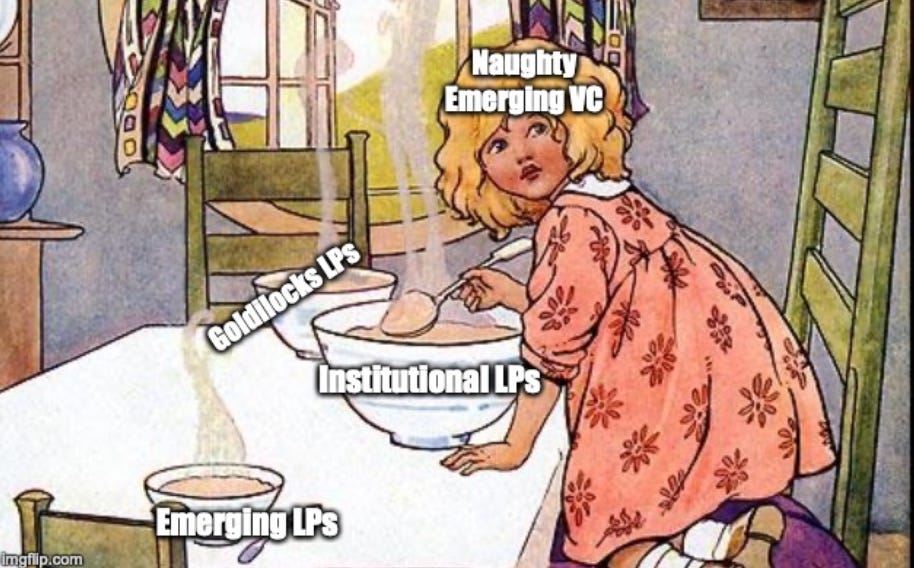

⏮Reverse fund-of-funds

Thousands of people have referenced Keith Rabois’ above tweet to highlight opportunities for new start-ups. Here’s one that people don’t often use this tweet for: VC funds.

If you’re Sequoia, Andreesen Horowitz, or Rabois’ Founders Fund, raising a new fund isn’t very difficult. These are storied funds with consistently strong returns. But they’re also special cases. Today, the “median” fund is not a Sequoia, but an emerging manager raising a new fund. In the past year alone, some estimate over 4,000 emerging managers have been raising for a new fund. Highly fragmented? Check.

When these emerging managers fundraise, they have to play a Goldilocks game. They can’t raise from large institutional LPs that Sequoia grabs for their multi-billion dollar funds. Our emerging VC’s $20m fund is just too small for the effort that would be required by these LPs. Large LPs look to invest $20m+ in a single check. Can our emerging VC go to a new class of emerging LPs? These emerging LPs are high net worth individuals passionate about start-ups and VC and want to help get new managers off the ground. A great solution! But these LPs write $5k-$50k checks. An emerging VC won’t necessarily want to round up 300 individual LPs. And even if they do, the SEC caps LPs into a VC fund at 99, so it’s actually just flat out illegal. So emerging managers have to find Goldilocks LPs - not too big, not too small, just right. Did I already say “check” for highly fragmented?

How about that NPS? Who’s happy about this setup? Spoiler alert: nobody.

🙁Small check LPs - Plenty has been written about the threshold to investing in VC as a barrier to wealth creation. AngelList has done wonders in making it easy for start-ups to open up their rounds to individuals writing checks as small as $1,000. Across the pond, Odin is working on something similar. However, investing in individual start-ups is of course not easy. Lots of people investing those $1,000 checks will lose that money. However, investing into VC funds is actually a safer way to gain access to one of the highest performing asset classes of this bull run. While an individual check likely won’t garner a 50x multiple that you might get investing directly into a start-up, it will be much less likely to garner a 0x multiple. And although investing into funds is safer, the threshold for investing is paradoxically higher. And many of these small check LPs may actually be more attentive and helpful to the emerging managers. But alas, they’re blocked.

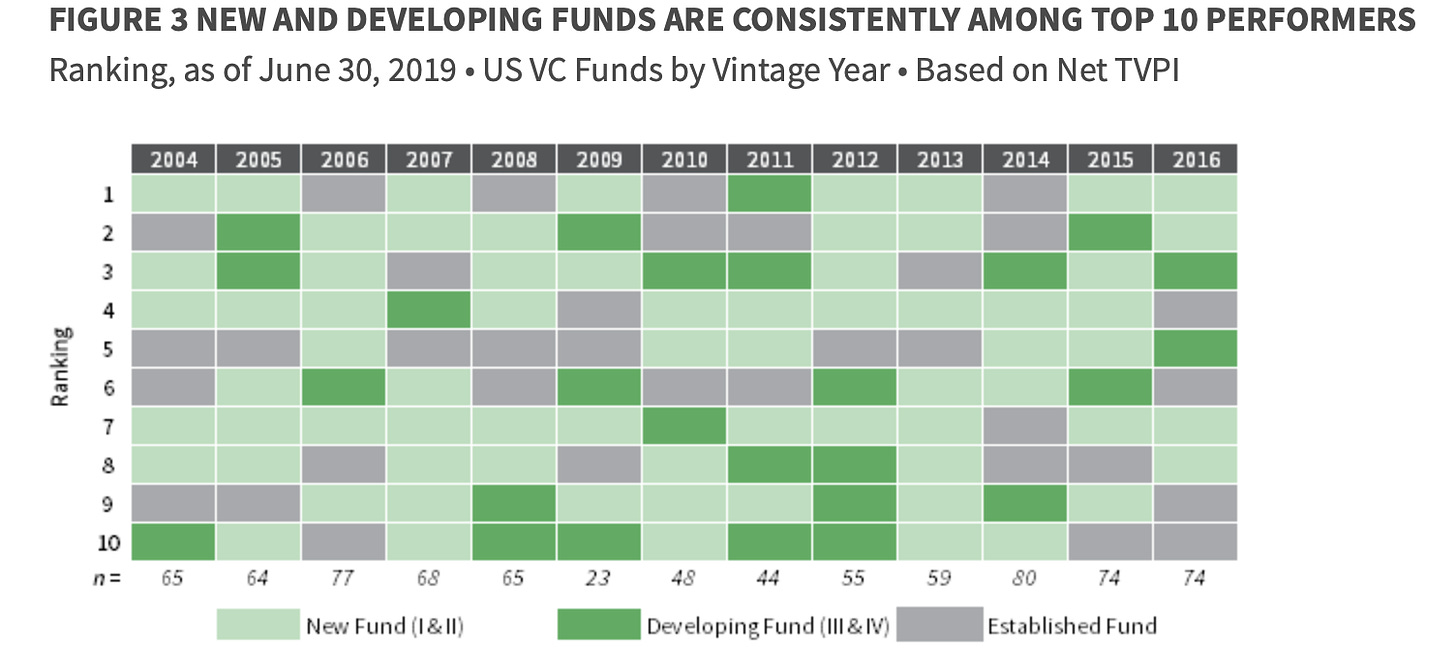

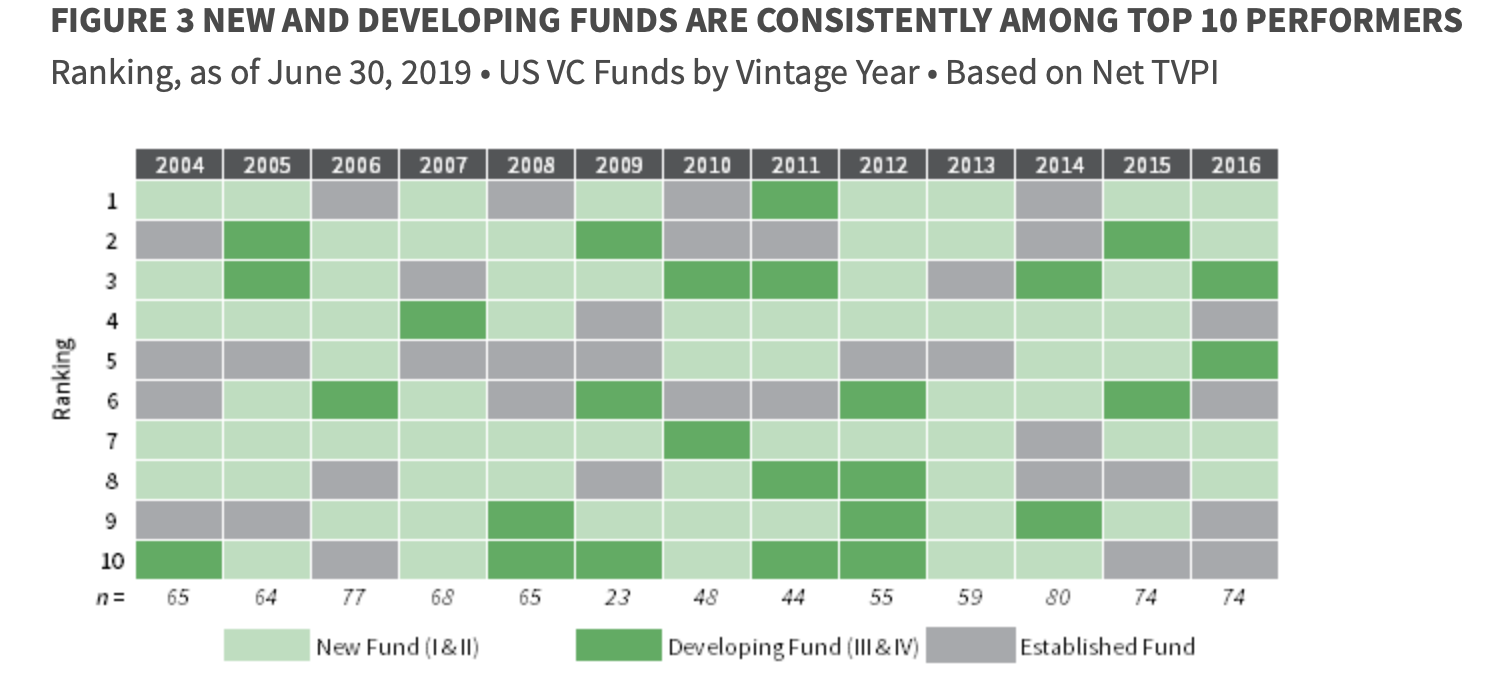

🙁 Institutional LPs - emerging managers have been one highest performing VC classes. In 8 of 10 vintages reviewed as of 2019, emerging managers (defined as Fund 1 or 2) have been at least 50% of the top 10 performing funds. Also in 8 of 10 vintages, an emerging manager has been the top performing fund. How can institutional LPs be satisfied with missing out on this class? The barrier remains that these funds are typically too small for institutional LPs to invest into so, for now, they are locked out.

🙁 Emerging Managers - The guardrails of “no more than 99 investors” and “your fund is too small for my effort” make an emerging manager’s fundraising job much more difficult. There are undoubtedly multiples more knowledgeable LPs interested in investing in emerging managers than can actually invest. Emerging managers have had to get creative to both bring in the small check LPs and the institutional LPs. On the small side, Packy McCormick set up a parallel fund structure to get around the 99 investor limit and allow more LPs to invest in his second fund. On the large side, one emerging manager I recently spoke to is teaming up with other emerging managers to create a separate, larger pooled fund that she calls a “reverse fund of funds.” Institutional LPs write large checks into the pooled structure that will eventually get split among the partner VCs. When things like this happen, the system is not keeping up with reality and opportunity arises.

Low NPS? Checks up the wazoo.

What’s required is a fund-of-funds targeted directly at emerging managers. This fund would accept investment from large and small LPs. For large LPs, unlock access to emerging VCs. For small LPs, give them access to the economic opportunity currently ring-fenced for a select few.

With a mix of ruthless process efficiency and technology to screen, vet, and invest in the most promising early stage investors, this fund-of-funds would be set to outperform the VC industry. Why? The last 10 years of fund returns have shown that there is no continuity in performance of a given fund from vintage to vintage, but emerging managers are classic outperformers.

Still hungry - they invest for the 20% carry, not the 2% management fee. They are incentive aligned to produce the biggest possible return on investment.

Differentiated offering - many of these new managers bring a unique skillset to their portfolio companies that move the needle for early stage companies much more than a VC’s brand.

Differentiated and focused thesis - these managers think about start-ups differently. They aren’t solely focused on SaaS or enterprise tech. They see the future in a way that many big name VCs cannot, and so are by nature contrarian.

I know of at least 4 different funds I would love to invest in. But I can’t because I either (1) don’t cross the minimum check threshold or (2) I do but can’t write that many checks into different funds because I’m not the monopoly man.

So are we starting this or what?

This stuck with me:

We can still have nice things:

Party on Wayne

— Nico

www.nicochoksi.com | @nico_in140

Did somebody send this to you? Sign up below to get the next one in your inbox: